Mutual Funds

Mutual funds are the best thing that you can do with your savings. Not only are they very simple to understand and invest in, they also offer the best returns over long term.

There are mutual funds available for all types of investment objectives. Whether you are planning to save for retirement or to buy a house in 10 years, Mutual Funds Sahi Hai!

What are Mutual Funds?

Mutual Funds offer you a way to invest your money through the help of investment experts.

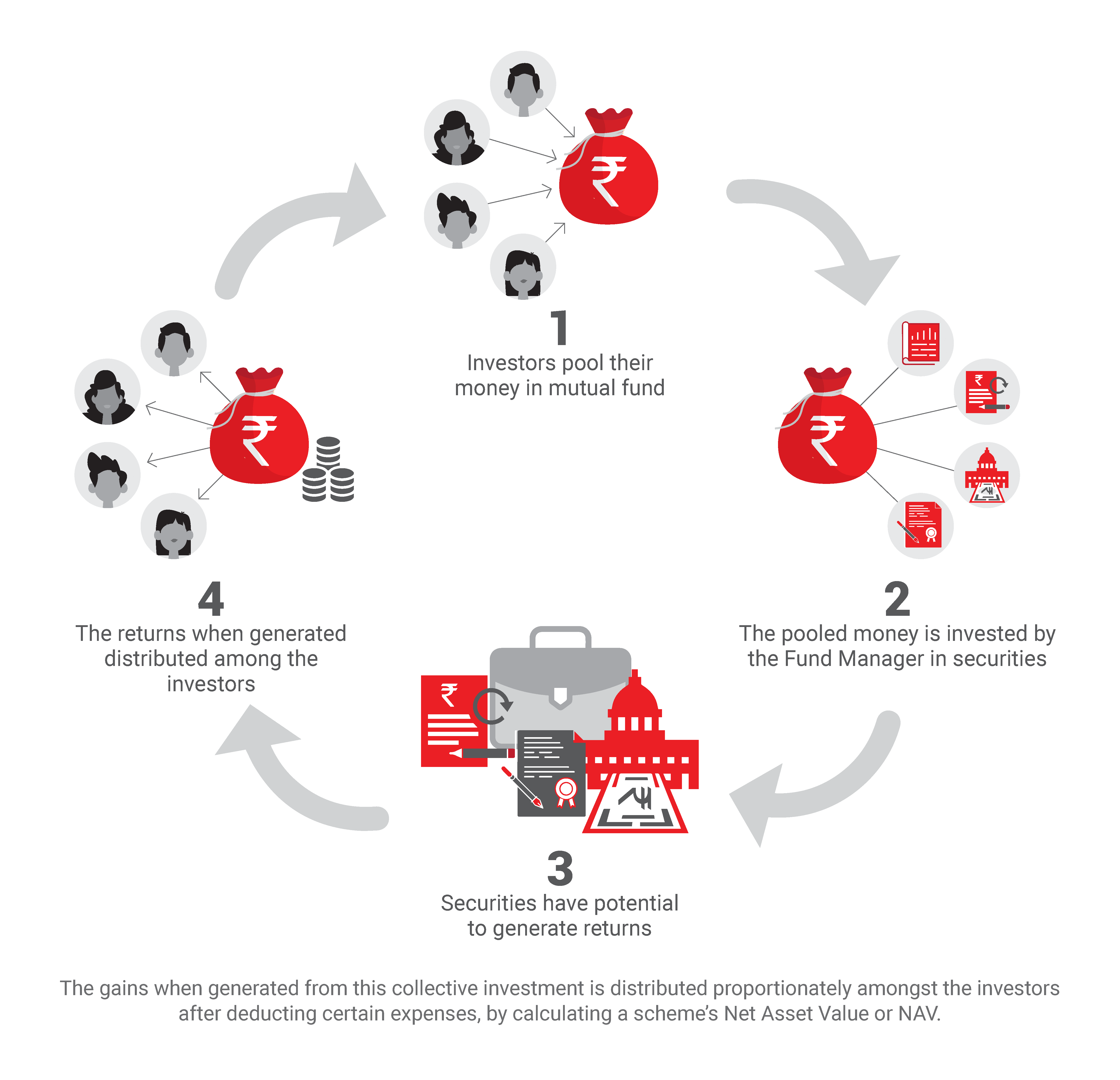

Simply put, it's a mechanism by which many investors pool their money. This pooled money is handed over to a fund manager to manage and grow systematically.

Depending on the type of mutual fund, this pooled money is then invested by the fund manager in either shares, bonds, money market instruments or a mix of all of them.

Total pooled amount is divided into units. When you buy a mutual fund of certain amount, you are allotted units of mutual funds which is equal to amount divided by the price. The price of a unit is called Net Asset Value or NAV.

Over time, as the price of the underlying investment securities (shares and/or bonds) increases, the NAV of your mutual fund unit also increases. When you sell at a higher NAV, you end up making money.

How does Mutual Funds work?

Why should you invest in Mutual Funds?

Mutual Funds offer a perfect balance of long-term returns, lower risk, fitment to your financial needs and liquidity.

Unmatched ease and simplicity

Investing in mutual funds is super easy and simple. And if you plan

to do it through an online platform, its also completely paperless.

Most of us do not have the required expertise to participate in equity markets. Mutual Funds give us a way by leveraging the expertise of a fund manager. You don't have to actively manage your investments.

Better long-term returns

In long-term, no other asset class has provided better returns than

equity. Equity as an asset class is the best wealth builder. If you

are looking to invest for long-term, equities are your best bet. And

what better way to invest in equities than letting a professional

fund manager do it for you.

Highly liquid

Another

important aspect of mutual funds is that they are highly liquid. You

can sell your units anytime and you get your money back. Liquidity

is important. Consider Real Estate for example. What if you are not

able to sell your property investment at the time you want money? No

such case with Mutual Funds.

Fits all financial needs

The beauty of mutual funds is that there is a type of mutual fund

for every type of financial need and investment objective. Looking

to save up for retirement or buying a house in 10 years or planning

to go on a vacation in 6 months or saving up for your child's

education? There are mutual funds available for all of these.

Different Types of Mutual Funds

Investment Objective

Suited For

Sub Categories

Taxation

Systematic Investment Plan (SIP)

SIPs have become a very popular term whenever one talks about

investments or about achieving financial goals. The AMFI’s “Mutual

Fund Sahi Hai “campaign has made this particular concept quite

popular and also left numerous new investors curious about investing

in this pattern. However, majority of the new investors are often

confused about SIPs.

Numerous investors confuse SIP as a

product and one often come across a query – “can I invest in a SIP

to achieve my goal?” SIPs are not synonyms for mutual fund schemes

but it is a very effective and efficient tool which helps one to

regularly invest in Mutual Fund Schemes.

Let’s clear the definition first.

What is a SIP?

A SIP is a tool to invest in

mutual fund schemes in a disciplined manner. SIPs allow an investor

to invest a pre-determined amount of money at fixed intervals in

selected mutual fund schemes. The amount can be as low as 100

depending on the requirement of the scheme and the interval can be

monthly/quarterly/semi-annually or annually. Sip help the investor

to safeguard its investments during high market volatility and also

stands to benefit due to low average costing and the power of

compounding.

What are the Benefits of SIP?

Brings In Discipline

Investing on a preset date every month, makes you set aside fixed sum of money to invest and gradually turns you into a disciplined investor.

Rupee Cost Averaging

You get more units when the markets go down and less when it goes up. Thus you average out the cost of buying mutual fund units.

Power Of Compounding

The longer you stay invested, more is the benefit of compounding. It is like earning interest on interest. Hence start an SIP early & enjoy the power of compounding.

Convenience

SIP offers convenience since you invest a small amount periodically without affecting your household budget.

No Need To Time The Market

No Need

To Time The Market Investing through SIP helps you avoid timing

the market.

Helps in Achieving Financial Goals

SIP is a smart tool that helps break your big goals into small amounts. Just ascertain the investment amount & start investing regularly through a SIP to achieve your dreams.

Flexibility To Select Investment Frequency

Select an investment frequency based on your convenience and need.

Any Drawbacks?

-

Averaged returns – If there is strong belief that

the markets would be positive in the coming periods then investing

lumpsum would be much more beneficial.

-

Less Control – Since one needs to invest a fixed

amount in a fixed chosen mutual fund if the investor changes his

mind then one needs to stop the first then start a new one if

there is limited source of investment amount.

- Cumbersome return’s calculation – Since investment is made every month one needs to get properly advised as to invest the optimum amount to get the desired financial result so there is always a need to consult a expert.

SIP vs Lumpsum Investment

| Basis | SIP | Lumpsum |

| Concept |

|

|

| Reason & Time to Invest |

|

|

| Pros |

|

|

| Cons |

|

|

| Suitability |

|

|

Let’s conclude with 2 important takeaways:

-

Stay Invested for a longer period – Investing for

a greater period is important as it helps to smoothen the risk

periods and periods of negative return and help the customers earn

better yield. Suppose a customer had started a SIP during 2015-16

when the markets were giving positive returns, but due to the

coronavirus pandemic shock the markets have come down considerably

so if the investor takes out his money now he will lose on to the

returns earned before and may even lose money due to the shock in

the market.

- Patience is the key – The most important thing of investing in SIP is to be calm and patient because the period of investing is huge and then only the good returns kick in so if a investor turns impatient and takes out his investments early he will lose out the high returns stored for him because the effect to compounding becomes more and more significant with each passing time period.

Mutual Fund - FAQs

▶ Are mutual funds safe?

The answer to this

question is both Yes & No. All investments are somewhat risky

because the market is unpredictable and is dependent on many factors

outside the control of the investor. There are many different types

of mutual funds that invest in different companies, in different

ways, and even in different proportions of equity and debt. Mutual

fund managers actively manage the investments of a certain mutual

fund scheme and monitor the risk and reward possibilities daily.

Mutual Funds also diversify your portfolio which decreases risk

automatically. All in all, Mutual funds are a safer place to invest

in, but not as safe as some investments with guaranteed returns such

as FD, MIS of Post Offices etc.

▶ How do I invest my money to make money?

Working hard is one way to make money, but to grow that money into

more money i.e. create wealth, one must invest it. To grow rich

faster than any traditional method of wealth generation, online

investment portals like ourselves allow users to invest quickly over

the internet with 100% security

▶ How do you make money from a mutual fund?

A mutual fund scheme invests in certain companies and

opportunities. When these invested companies perform well, or the

opportunities pan out in a positive way, the fund scheme earns a

share of that prosperity. The share so earned is then divided

amongst all investors in proportion to their investment.

▶ How much money do you need to start investing in a mutual

fund?

You can start investing in mutual funds and SIP with as little as ₹

1,000.

▶ How much should I invest in mutual funds?

How much to invest in mutual funds largely depends on three

factors:

- How much you have available to invest after deducting living expenses.

- How much risk you are willing to undertake.

- For how long you wish to remain invested.

Experts recommend investing 80% of your monthly surplus (amount remaining after deducting for monthly living expenses) into mutual funds either through lump sum or SIP.

▶ Is it a right time to invest in mutual funds?

It is always the right time to invest in mutual funds. You may have

heard of fund managers and investors waiting to “time the market”

correctly before they make their investments – but at any given

time, there will be certain funds performing poorly and certain

funds performing exceptionally well.

Also, in the case of SIPs - the benefits of Rupee Cost Averaging and regular investment instalments means that timing the market is of little importance.

▶ What are the benefits of a mutual fund?

- Mutual funds investment can multiply your wealth.

- Minimal risk as compared to other investments.

- Portfolio diversification is possible - meaning that you don’t put all your eggs in one basket.

- More chances of success and profitable returns thanks to investment diversification.

- Mutual funds are actively managed and employ a professional fund manager whose performance parameters are directly linked to the performance of the fund scheme.

Investments in a mutual fund through a particular AMC can be switched - meaning that the investment can be redirected into another mutual fund scheme at any time depending on market conditions.

- ELSS investments can help you save up to ₹ 1,50,000 from taxation under Section 80C.

- Mutual funds provide higher potential returns than any other type of investment avenue.

- Mutual funds can be invested through a method called SIP - Systematic Investment Planning - which carries a host of benefits to the investor.

▶ What is the average return on mutual funds?

There are thousands of mutual fund schemes that offer varying

levels of returns. Usually, the higher the returns, the higher the

risk being undertaken. The returns of a mutual fund scheme vary

based on many other factors as well, but the average returns

generated over a certain period of time, say, 5 years, is much

higher than other investments with similar lock-in periods such as

FDs.

Mutual Funds are companies that bring together a group of

people and invests on their behalf.

▶ Why Mutual Funds?

- Diversification -'Don't put all your eggs in one basket' Concept.

- Professional Management - Qualified professionals with research teams manage your funds.

- Transparency - Sharing account statements, factsheets and declaring NAVs daily.

- Regulation - Funds follow strict regulations to protect investors.

- Rupee Cost Averaging - Your money buys more units when markets are low and vice-versa.

- Liquidity - Redeem your investments with convenient payout options.

▶ How to Invest in SIP?

As an investor,

you need to set your investment goals and then choose the fund as

per your risk appetite and return requirements. We at Richfield

Fintech will prepare a risk profile basis your inputs and will take

proper care of every penny invested with us.

▶ How to choose a SIP?

Due to

Mutual Funds being such a hype, the internet provides you with

innumerable options and a prudent investor must shun the noise and

focus on his/her goal-based needs. We will help you provide data

points on all the available funds along-with some top highlights

which keep updating every few months depending upon the market

cycle.

▶ How much should I invest in a mutual fund through SIP?

It totally depends on your income and the financial goals you have

set you can start with an amount as moderate as 500.

▶ Can a SIP payment be missed?

The account

won’t be deactivated even if you miss your payments. You can also

pause your SIPs in case of an emergency.

▶ Are SIPs tax exempt investments?

Only

Investment done in ELSS mutual funds through SIP are tax exempt

under Sec 80 C.

▶ Is SIP safe?

SIP is just another mode of

investment. The safety is measured on the basis of the mutual fund

chosen.

▶ Does SIP mean invest only in Equity funds?

There is a great misconception that investing in mutual fund is

investing in equities and the same is felt about SIPs. But SIPs can

be made in equity, debt or hybrid schemes depending on the risk

appetite of the investors.

▶ When is the best time to invest in SIP?

When

it come to the markets you can never time them so going by the rupee

cost averaging logic, anytime is the best time to invest. In fact in

time value terms, earlier you start, larger is your wealth creation.

Partner AMCs

You request has been submitted. You will be contacted soon.