WALL STREET

While one can argue that Foreign Institutional Investors are always on the lookout for investing in Developing Countries and India is one of their favourite spots because of the large growth potential it offers along-with favourable demographics. But let’s be honest counties like USA, Japan, UK have far more developed Equity Markets -and now Indian residents can easily invest in foreign equities.

Why Invest in Wall Street

While one can argue that Foreign Institutional Investors are always on the lookout for investing in Developing Countries and India is one of their favourite spots because of the large growth potential it offers along-with favourable demographics. But let’s be honest counties like USA, Japan, UK have far more developed Equity Markets and the primary reason is that they had a head start. The origin of NYSE is dated back to May 17,1972 and Tokyo Stock Exchange was established on May 15, 1878. Even in terms of Market Capitalization, India is far behind global stock exchanges. (Market capitalization is the measure of corporate size of a country. It shows the current stock price multiplied by the number of outstanding shares. It is commonly referred to as Market cap).

World Stock Markets and their Market Capitalization

| Sr. | Country | Stock Exchange | Market Cap (In Trillion $) |

| 1 | USA | NYSE | 19.3 |

| 2 | USA | NASDAQ | 13.8 |

| 3 | JAPAN | TOKYO STOCK EXCHANGE | 5.7 |

| 4 | CHINA | SHANGHAI STOCK EXCHANGE | 4.9 |

| 5 | HONG KONG | HONG KONG STOCK EXCHANGE | 4.4 |

| 6 | EUROPE | EURONEXT | 3.9 |

| 7 | CHINA | SHENZEN STOCK EXCHANGE | 3.5 |

| 8 | UK | LONDON STOCK EXCHANGE | 3.2 |

| 9 | JAPAN | TORONTO STOCK EXCHANGE | 2.1 |

| 10 | INDIA | BOMBAY STOCK EXCHANGE | 1.7 |

-Source: Business Insider (June 2020)

And while we are comparing the world stock exchanges and their market cap, one must also look at Tech which has continued to dominate the global stock markets despite Covid-19 disruptions as the combined market cap of Seven FANGMAN stocks- Facebook, Amazon, Netflix, Google, Microsoft, Apple, Nvidia is $6.4 Trillion which is more than the GDP of several countries. One of the common answers to a “Which stocks should one invest in?” has been that one should invest in the stocks of the companies whose products they themselves use and know that these companies have a large market share, if not already a monopoly. So, when you talk about FANGMAN, each and every one of us uses the products of these companies in one way or the other. A lot of people have the same question all over the internet. How do I invest in Amazon, in Google etc.? Is it legal? It must only be for HNIs but for me as a retail investor, it shouldn’t be possible right? Will I be taxed Twice, once in USA and once in INDIA?

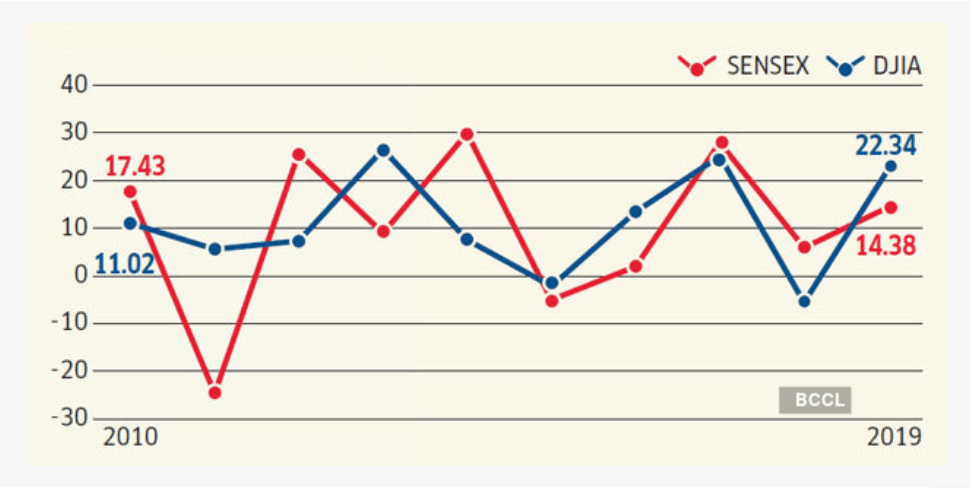

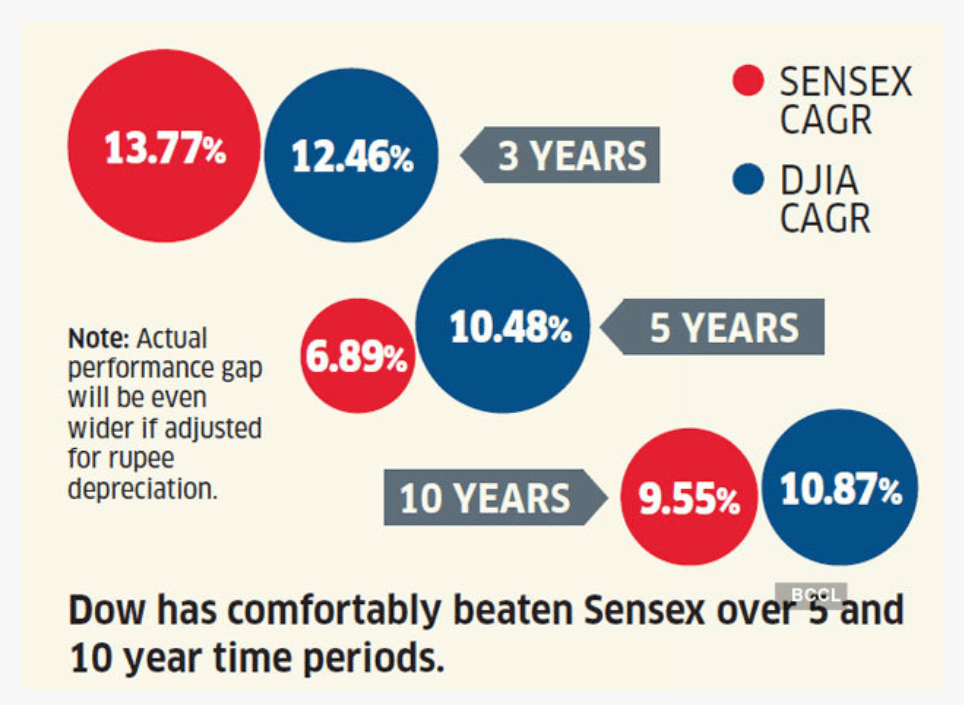

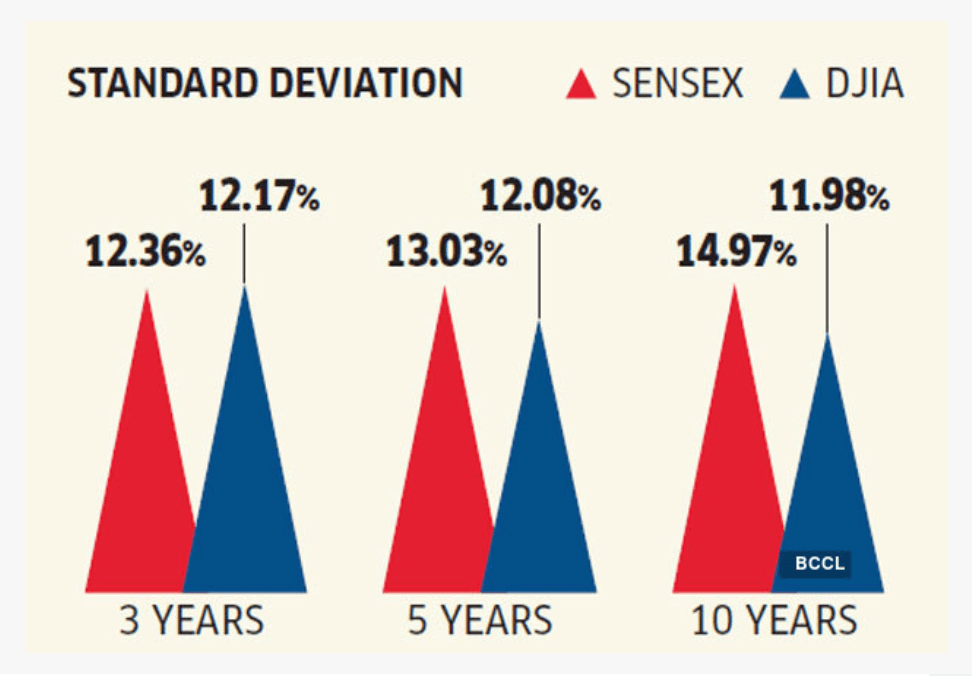

Historically Wall Street offers better returns

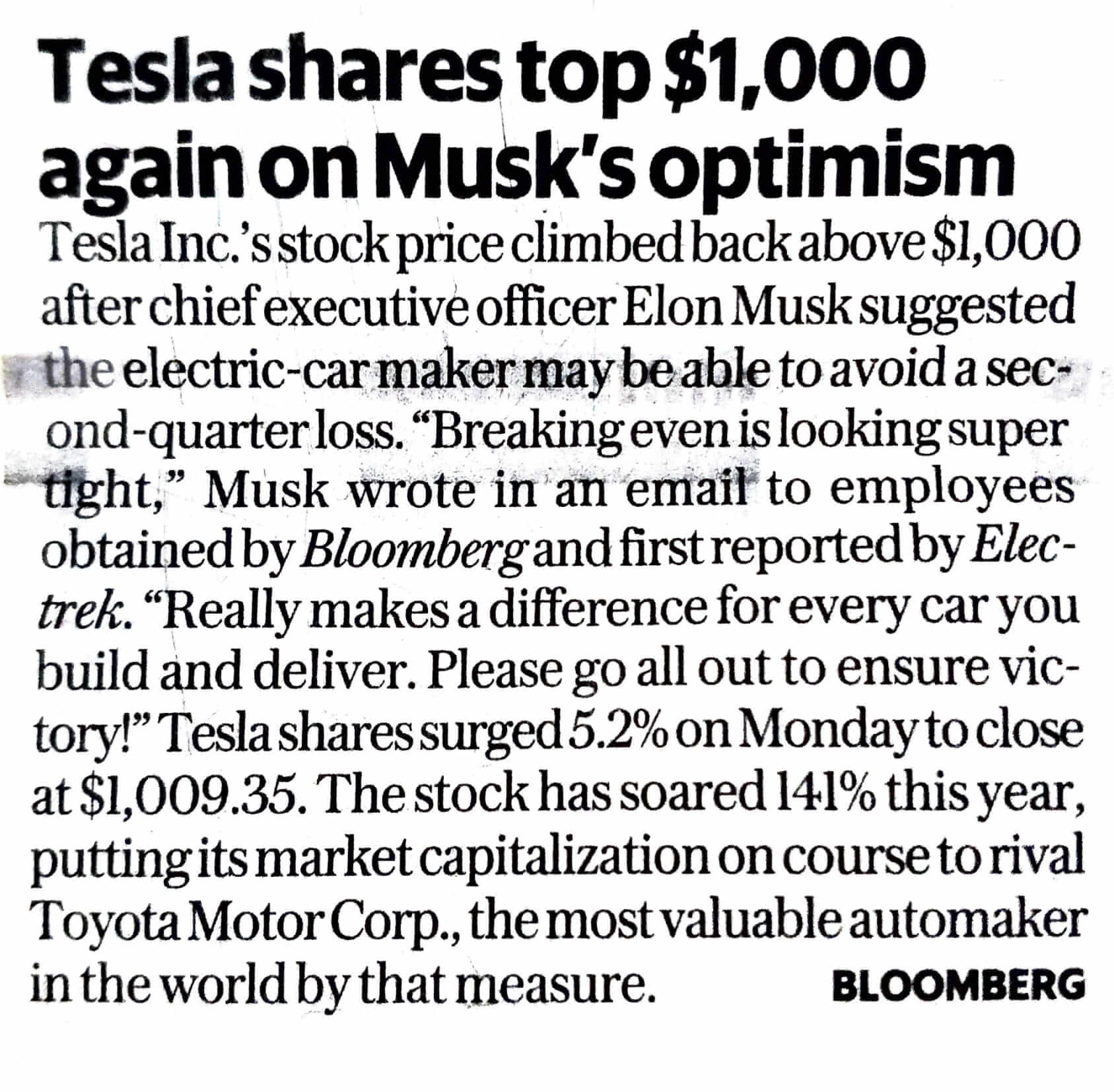

Wall Street News

How to Invest in Wall Street from India?

Yes, an Indian resident is allowed to remit upto $250,000 per year under LRS (Liberalized Remittance Scheme) of RBI. That $250,000 can be used for any purposes out of India - including investments in foreign equities.

Secondly, Will I be Taxed Twice? Once in US and once in India?- Yes, tax needs to be paid on Foreign dividend both in US and India. However, an Indian Resident individual can claim Tax credit of taxes paid in US by virtue of Double Taxation Avoidance Agreement (DTAA) entered into between India and US by filing a return of income in India. Maximum credit that can be availed is the amount of tax that should have been paid in India on the transaction if there is no DTAA. However, Capital Gain Tax on Transfer of Securities needs to be paid only in India.

Today, the most widely available way to invest in Global Equity is via Mutual Funds. For ex. Parag Parikh Long Term Equity Fund, Nippon India US Equity Opportunities Fund etc. but there are 3 cons of investing in these mutual funds vis-à-vis investing in direct equity route:

-

Cost Effective- The International Mutual Funds category have an

expense ratio of over 2.7% wherein investing via direct equity

route can save upto 1% of that cost depending on the amount

invested. In percentage terms, higher the amount invested lower

the expense ratio.

-

Taxation- International Mutual Funds are regarded as debt funds

and are taxed at slab rate if your holding period is less than 3

years after which long term capital gain (LTCG) tax of 20% with

indexation is applicable. However, if one invests in Direct

Equity Route then the same is treated as Unlisted Equity and the

holding period for it to be taxed at LTCG rates of 20% with

indexation reduced to 2 years.

- Dependency- Mutual Fund as a category invests at the discretion of the fund manager and the investments keep churning along-with diversification factors like sector allocation. Since, investing in foreign equity itself is a diversification one may want to limit their risk towards the branded equity stocks like Amazon, Netflix, Apple etc. but the option of choice is not provided in Mutual Funds whereas it is readily available in Direct Equity Space.

Thus, we offer you a chance to invest in those sophisticated

markets and own a portion of the FAANGMAN

(Facebook-Apple-Amazon-Netflix-Google-Microsoft-Adobe-Nvidia)

stocks, products of which companies have become an integral part

of our daily lives and more, providing for diversification in

one’s portfolio at minimal cost.

Start investing in Wall

Street from India securely and online - here.

Where to Invest in Wall Street?

FAQs on Wall Street Investing

▶ How does it work (Modus Operandi)

Once

you’ve logged into your account, click on the “Invest Abroad”

option given to you and you will be redirected to our American

Partner’s Website Stockal where you’ve to create an account

filling in basic details like name, email etc.. Your brokerage

account is, in turn, automatically created with DriveWealth - for

clearing and brokerage services. It will take 2 business days for

your account to get approved. Once approved, you will have to fund

the account by transferring money into the brokerage account from

your bank account. Once the funds become available in your

brokerage account, you will be able to make investments globally

(currently supporting USA only). Feel free to use the extensive

research and support available on the platform. After selling any

of your investments, whenever you want to get your money back,

just click on "Withdraw" and all your available cash will be sent

over to your domestic bank account.

▶ What are the documents required for opening an account?

Any one of the following documents for a combination of Picture

ID proof + Proof of address Picture ID proof:

- Government issued Photo ID (voter id, PAN card)

- Valid driver’s license

- Passport

- Voters registration card and photo

Proof of address:

- Utility bill

- Mobile phone bill, bank or credit card statement

Else, any one of the below documents would suffice, picture ID proof of address:

- Valid driver license with address

- Government issued Photo ID with address (Aadhar card)

▶ How do I add funds to my trading account?

Just click on the "Add funds" button available on Stockal

(partner website). Enter the amount you want to send to your

brokerage account. A pre-filled LRS form (more on LRS later) will

be presented to you. Verify the information and download the PDF

of the form from the website. You will need to, either just sign,

scan (or click a pic), and upload it back. Easy instructions will

be available alongside the LRS form.

▶ How do I withdraw money back to my account?

All you need to do is click the "Withdraw" button on your

Portfolio page or inside "My Account". You will be shown how much

money is available for you to withdraw. This is the "cash" in your

account - either uninvested money or generated from sales of

securities you, previously, owned. You can place a withdrawal

request and the money will be wired to your domestic bank account.

It takes 4-5 business days for the money to hit your account. Any

request above $10,000 requires an additional email approval. There

is a $35 fee associated with withdrawals, charged by the US bank,

so the cash balance in your account should be at least $35 at the

time of placing the withdrawal request (You can find the Detailed

Fee Structure below)

▶ Is there a minimum amount that I need to invest?

No. Unlike most traditional investing platforms, we place no

restrictions on user accounts. Having said that, in order to see

benefits of investing accrue to you, we recommend that you

invest at least $1000 to start off.

▶ Where is my US investing account held?

Your investing (brokerage) account is opened at our US

brokerage and clearing services partner DriveWealth - a FINRA

regulated brokerage firm. It is a licensed carrying and

self-clearing broker offering brokerage services to global

investors. DriveWealth is backed by Softbank Group and other

leading venture capital firms in the financial services ecosystem.

The custody of your account, in turn, would be held by DriveWealth

one of their custodian partners.

▶ How do fractional shares work?

One of the

unique things about the US stock markets is that investors can own

fractions of stocks. Unlike in countries like India. So you could

own 0.05 of Apple stock. Our brokerage partner DriveWealth allows

you to own as low as 0.0001 share of any stock. And this is great

for 2 reasons: You don't have to think in terms of "how many

shares should I buy?". You can simply decide to invest a certain

amount of money and the number of units to be allocated to you

gets automatically calculated and would get credited to your

account. For instance, if a stock is valued at $27 and you decide

to invest $100 in it, you will get 3.70 shares. Many popular US

stocks are more expensive than typical Indian stocks. While a

single Apple stock is valued at over $200 as of this writing,

Google costs over $1,250 and Amazon costs more than $2,250. Pepsi,

Nike, Coke - all between $100 and $200. As of this writing. So,

with fractional stocks you could effectively build a pretty

diversified portfolio with small amounts of money.

▶ Do I get voting rights on fractional stocks? And what

about dividends?

You don't get voting rights on fractions of stock you own.

So if you own 34.5 stocks of a company, your voting rights will be

for 34 shares. Dividends, yes! If a hundred dollar dividend per

share is announced, you will get $3,450. The only limitation is

that we cannot give you fractional money so if you own 0.0001

stock and the dividend announced is $5 per stock, you will not be

able to receive half a cent.

▶ Who is the custodian of my account?

DriveWealth the custodian, works with Citigroup, New York,

for the custody of brokerage accounts.

▶ What is the safety-net on my account? What if Stockal goes

down?

You global investing accounts are held by brokerage and

clearing services providers. The custody of your account is

managed by some of the largest banks and clearing firms in the

world. If Stockal goes down, your account will still be safe and

secure with them and you will be able to access it and/or move it

to another brokerage firm as you please. Additionally, you also

have automatic insurance on your US investing account US brokerage

ecosystem recommends that ever investor account should have

insurance. The brokerage partner, DriveWealth, is a member of the

Securities Investor Protection Corporation (“SIPC”) which

currently protects the securities and cash in your Account up to

USD 500,000 of which USD 250,000 may be in cash. Please note that

this USD 500,000 is not applicable general losses in the stock

market. SIPC says the following: SIPC protects against the

loss of cash and securities – such as stocks and bonds – held by a

customer at a financially-troubled SIPC-member brokerage firm. The

limit of SIPC protection is $500,000, which includes a $250,000

limit for cash. A non-U.S. citizen with an account at a brokerage

firm that is a member of SIPC is treated the same as a resident or

citizen of the United States with an account at a brokerage firm

that is a member of SIPC. SIPC does not protect against the

decline in value of your securities. SIPC does not protect

individuals who are sold worthless stocks and other securities.

SIPC does not protect claims against a broker for bad investment

advice, or for recommending inappropriate investments. Explanatory

brochure available upon request or at www.sipc.org.

▶ Who owns the stocks?

You own the stocks through your account with Richfield

Fintech powered by Stockal and DriveWealth. DriveWealth manages

the books and records and stocks are held in custody by ICBC

Financial Services, New York.

Miscellaneous Charges

- $20.00 Returned Checks

- $25.00 Check Stop Payments

- $20.00 Overnight Check Delivery

- $25.00 Returned Wire Transfers (applies to attempted third-party wires)

- $5.00 Tax Certification (W-8 Ben). One-time fee upon a non-US account opening

- $50.00 1099 Request for Exempt Accounts

- $25.00 Tax Document Request (Fax and Regular Mail)

- $3.00 Physical Copy of Trade Confirmations (per confirmation)

- $5.00 Physical Copy of Monthly Account Statement (per statement)

Withdrawal/ Administrative Request Charges

- $3.00 Paper Check / e-check (USD)

- $0.25 ACH Transfer (outgoing)

- $25.00 Outgoing Domestic Wire Transfer

- $35.00 Outgoing International Wire Transfer

▶ Which stock markets are available to invest in?

Currently, our Partner Platform -Stockal helps you invest

in US stock markets. In another three months, we will have

multiple other markets available - Germany, Japan, India, UK and

Hong Kong. Over time, we will make investing totally ubiquitous -

if you have an idea or come across a company you want to invest

in, you will be able to make that investment without having to

think if that stock is listed domestically or in some other

country. Interestingly, many large global companies have US listed

ADRs which are available with us. From Chinese giants like Alibaba

to many Indian and European companies are all available.

▶ Which are the countries from where investments can be

made?

Our partner Platform Stockal is currently available to

investors in India and most of the countries in Middle East &

North Africa (MENA). We will shortly become available to investors

in other South East Asian Countries.

▶ How many securities are available to invest in?

Currently we offer 3000+ securities - listed on NASDAQ and

NYSE - as of now. These are a mix of stocks and ETFs (Exchange

Traded Funds). Almost all the marquee listed companies in the US

with USD Billion+ market caps, are available.

▶ How much can I invest in US stocks from India?

Currently, you can invest up to USD 250,000 every year in foreign

stocks from India. This amount can change, subject to RBI

guidelines. So your investments in US securities are also governed

by the same limit. Foreign investments fall under clearly defined

RBI guidelines. The remittance of money for foreign investments

comes under the Liberalized Remittance Scheme (LRS). Under LRS an

Individual can remit up to USD 250,000 per financial year to

invest in foreign equities done through an authorized dealer

(commonly, your bank). As per RBI policy, having a PAN card is

required to purchase shares in foreign countries.

Disclaimer: This article is for informational purposes only. None

of the contents of this article should be treated as tax advice.

Please consult a qualified tax consultant or expert with your

specific taxation situation for appropriate advice.

▶ What is LRS?

Instituted by the RBI, the

Liberalised Remittance Scheme or LRS is a set of policies that

stipulates the maximum amount and purposes of remittance. Under

the LRS, an individual can annually invest up to USD $250,000 in

any country, without seeking approval from the RBI. To monitor the

remittance of individuals, remitters are required to fill out and

submit a Form A2, which is provided by RBI-appointed Authorized

Dealers. The form captures the remittance amount, the purpose, and

the individual’s PAN number. Once the form is received, the

Authorized Dealer will verify the information and process the

remittance. The authorized dealer in this case is the bank which

has been chosen for remittance.

▶ What are the documents required to transfer money to invest

out of India?

The following documents are needed: Form A2 along with a

declaration form: As per FEMA, required every time the money is

sent abroad to declare the sum amount that is to be transferred.

Your bank will file this for you within the LRS filings. Stockal

automatically fills this for you - all you need to do is, make

sure that the information is correct, then download the filled-in

form, sign and upload it back for your bank to file. Bank KYC

documents: PAN card and your address proof.

▶ Is there any tax implication on transfer / remittance of

funds into your platform for making investment in foreign

securities?

Transfer of funds into an external platform would not

result in any profit/gain as it involves only transfer of funds to

self. Further no transaction has been undertaken / executed

resulting in any transfer of any asset. However, w.e.f. 1st

October 2020, any foreign remittance by resident individuals under

Liberalised Remittance Scheme framed by RBI may trigger TCS (Tax

Collection at Source) provisions which requires collection of tax

by an authorised dealer at 5% (10% in case of non-PAN / Aadhar

cases) where the total foreign remittance including transfer of

funds exceeds ₹ 7,00,000 per annum. In this regard, transfer of

funds into our Partner Platform Stockal by way of foreign

remittance may attract TCS. However, it is pertinent to note that

AD would be liable to collect TCS @ 5% on the amount exceeding ₹

7,00,000.

▶ What is the definition of Long-term Capital Asset (LTCA) and

Short-term Capital Asset (STCA) w.r.t foreign listed securities?

What are the tax rates if any capital gain (Long term or Short

term) is accrued on sale of such Capital Assets?

The time period for which a particular capital asset is

held by its owner decides whether that asset is a short-term

capital asset or a long-term capital asset. Shares of a company

listed on foreign stock exchanges (are considered as unlisted

securities for Income Tax purposes) shall be considered as LTCA if

the same is held for more than 24 months while those held for 24

months or less shall be considered as STCA. Tax rate with respect

to LTCG and STCG applicable on Indian resident has been provided

below Capital Gains Tax Rate:

| Particulars | Tax |

| Short Term Capital Gains | Slab rates (Plus applicable cess and surcharge) |

| Long Term Capital Gains | 20% (Plus applicable cess and surcharge) |

▶ Am I liable to pay tax when I remit the funds back to

India?

No, the tax incidence is on the event of transfer of

securities by the Client on our Partner Platform Stockal i.e. Tax

Incidence is on the Purchase/Sale of Securities. The remittance of

any funds lying outside India has no connection with the tax

incidence.

▶ Can I set off the losses incurred on transfer of foreign

listed securities with my other income in India?

All Short-term capital losses arising on sale of foreign

listed securities can be set off against both short term and

long-term capital gains in India. However, any long-term capital

loss arising on sale of foreign listed securities can only be set

off against long term capital gains in India. (Assuming there is

no intraday trading)

▶ Can I carry forward the losses incurred from dealing in

foreign listed securities under Income Tax Act?

Yes. The losses arising from the sale of foreign listed

securities can be carried forward up to eight consecutive years

while losses from speculative business can be carried forward for

a period of 4 years.

| Losses | Can be Set off against | Can be Carried Forward up to |

| STCL | STCG or LTCG | 8 years |

| LTCL | LTCG | 8 years |

| Speculative business loss | Speculative Income | 4 years |

▶ Can I take indexation benefit on transfer of foreign listed

securities?

Indexation is a benefit given to adjust the cost of capital

asset held for long term with respect to inflation. Since foreign

securities are considered as unlisted, they must be held for at

least 24 months to qualify as Long-Term Capital Asset and avail

indexation.

▶ Is there a limit on maximum number of foreign securities to

be held by an Indian Resident?

There is no maximum limit on the number of foreign securities

that can be held by an Indian resident. However, under the LRS

(‘Liberalized Remittance Scheme) an amount up to USD 2,50,000 per

resident individual can only be remitted outside India in one

financial year (April – March).

▶ Can a Resident Indian utilize more than the amount specified

(USD 2,50,000) under LRS for buying foreign listed

securities?

An Individual cannot remit more than USD 2,50,000 in one

financial year under LRS scheme however, a resident individual

investor who is not permanently resident in India after having

remitted their entire earnings and salary, wish to further remit

other income over and above the limit of USD 2,50,000, may

approach RBI with documents through their AD bank for approval.

▶ What is the tax on dividend received from foreign listed

securities?

Interest received from foreign debt instruments will be

subject to tax at normal slab rates for the Individuals and at

applicable rates to Body Corporates as Income from Other Sources.

▶ Do I need to pay tax on foreign dividend both in US and

India? Can I claim credit for the taxes paid on such dividend in

India?

Yes, tax needs to be paid on Foreign dividend both in US

and India. However, an Indian Resident individual can claim Tax

credit of taxes paid in US by virtue of Double Taxation Avoidance

Agreement (DTAA) entered into between India and US by filing a

return of income in India. Maximum credit that can be availed is

the amount of tax that should have been paid in India on the

transaction if there is no DTAA.

▶ Am I expected to report my holdings or gains in India an

annual basis - even if I don't have a tax liability? If yes,

under what section and what forms do I need to report the same

in India?

Where a person is a ROR he/she is required to file his/her

income tax return if the person has any kind of foreign assets.

The reporting in this regard would be as follows:

- Details of foreign assets and income from any source outside India –Schedule FA of the relevant Income Tax Return (ITR).

- Details of Income from outside India (only in the case of resident and ordinarily resident) – Schedule FSI of the relevant ITR.

▶ Can I claim the fees and brokerage paid as a deduction for

computing my capital gains tax in India?

Yes, any cost incurred on account of sale or transfer of

asset is allowable as a deduction while computing the Capital

Gains. However, it is pertinent to note that AUM charges and

annual subscription charges incurred cannot be claimed as

deduction as they are related to holding of capital asset and not

in relation to transfer of capital asset.

▶ What are the tax implications in India where my shares get

vested with my nominee in case of my death?

There is no applicable estate duty in India on vesting of

properties with the nominee in the event of death.

▶ What are the TCS provisions (including thresholds, if any)

regarding the overseas investment made by an investor?

As per Finance Act, 2020, TCS @ 5% is applicable only if and when

the foreign remittance in a Financial Year exceeds ₹ 7,00,000. It

is pertinent to note here that TCS provisions on foreign

remittance are applicable from 01-10-2020.

▶ What are the tax implications in India if I am a Non-Resident

Indian (NRI) residing in any country other than USA?

Irrespective of the country where NRI resides, any income of a

non-resident is chargeable to tax in India if it is accrued or

received in India. As per ITA, deduction of expenditure or

allowances is not available while computing investment income or

long-term capital gains. Also, indexation benefit is not available

to an NRI while computing LTCG. It is to be noted that earning

Capital Gains on our Partner Platform Stockal is not liable to tax

in India. Special Tax Rates:

- Investment Income: 20%

- Long Term Capital Gain: 10%

You request has been submitted. You will be contacted soon.

'Risk comes from not knowing what you are doing'

-Warren Buffett

Disclaimer

All investments involve risk and the past performance of a security, or financial product does not guarantee future results or returns. Keep in mind that while diversification may help spread risk it does not assure a profit, or protect against loss, in a down market. There is always the potential of losing money when you invest in securities, or other financial products. Investors should consider their investment objectives and risks carefully before investing. Investors should be aware that system response, execution price, speed, liquidity, market data, and account access times are affected by many factors, including market volatility, size and type of order, market conditions, system performance, and other factors.

Richfield Fintech makes no warranties or representations, express or implied, on products and services offered through the platform. It accepts no liability for any damages or losses, however, caused in connection with the use of related services.

All information placed on Wall Street Investing website is for informational purposes only and does not constitute as an offer to sell or buy a security. Further, any information on the website is not intended as investment advice. Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with Richfield Fintech with respect to any linked site or its sponsor, unless expressly stated by Richfield Fintech . Any such information, products or sites have not necessarily been reviewed by Richfield Fintech and are provided or maintained by third parties over whom Richfield Fintech exercise no control. Richfield Fintech expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

Richfield Fintech role here is limited to a Referrer. Richfield Fintech will introduce the customer with the platform provider Stockal post which clients will be directly sharing their details to third party stock broker Drive Wealth. Once customers have been referred, they are solely responsible for any and all orders placed by them, and understand that all orders are unsolicited and based on their own investment decisions. Richfield Fintech and any of its employees, agents, principals, or representatives DO NOT: provide recommendations of any security, transaction, or order; provide investment advice; produce or provide research to any user regarding any security, transaction, or order; handle funds or securities related to securities orders or effect the clearance or settlement of a user’s trades done through Global Investing.in solution provided by Stockal Inc. and DriveWealth LLC. All processes including KYC will be executed by Drive Wealth & Stockal directly with client and Richfield Fintech will not incur any personal financial liability.

Investment in securities market are subject to market risks, read all the related documents carefully before investing. Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Richfield Fintech is a financial services intermediary and is

engaged as a distributor of financial products & services like

Corporate FDs & Bonds, Insurance, MF, NPS, Real Estate

services, Loans, NCDs, IPOs, E-Will & E-Tax in strategic

distribution partnerships. Customers need to check products &

features before investing since the contours of the product rates

may change from time to time. Richfield Fintech is not liable for

any loss or damage of any kind arising out of investments in these

products. Investments in Equity, Currency, Futures & Options

are subject to market risk. Clients should read the Risk

Disclosure Document issued by SEBI & relevant exchanges &

the T&C on www.richfieldfintech.com before investing. Equity

SIP is not an approved product of Exchange and any dispute related

to this will not be dealt at Exchange platform.

All logos and

trademarks belong to their respective legal owners.

Check the

background of DriveWealth, LLC on FINRA’s Brokercheck here. Under SIPC, all securities accounts are protected up to

$500,000 (including $250,000 for claims on cash). More details

available here.